Key Takeaways

- AI products now represent 42% of revenue at surveyed companies, projected to cross 53% majority threshold by 2027

- Open source models reached 40% adoption at the app layer while frontier API usage slipped from 85% to 80%

- 66% of builders rank agentic AI as their top investment priority, yet only 5% say agents rarely need human intervention

ICONIQ just dropped the third edition of its State of AI report, titled "The Builder's Economy," and the thesis has shifted hard. Six months ago, the conversation was about proving AI works. Now it's about proving AI pays. The Q2 2026 survey of 305 software executives building AI products shows AI revenue approaching half of total business, margins expanding to 53%, and a clear pattern: the companies pulling ahead treat pricing, cost, and org design as product decisions, not afterthoughts.

Several numbers also reversed from the January report. That makes this a useful moment to reset your assumptions about where the market actually stands. Here are the 10 metrics that matter.

Frontier labs vs open source: the real model story

The provider rankings reshuffled fast. Anthropic overtook OpenAI as the most-used provider, jumping from 51% in Q4 2025 to 81% now. OpenAI sits at 71%, Google at 50%. But that's a subplot. The average builder runs 3.3 providers, so no single lab is the story.

The real story is the category fight. Licensed frontier APIs still lead at 80%, but that's down from 85%. Open source climbed to 40% from 37%, now edging past proprietary in-house models at 37%. ICONIQ expects open source to keep gaining as cost and control advantages compound. The fork for builders isn't which frontier lab to pick. It's whether to rent frontier intelligence or run open models you control.

Here's the unexpected part: 58% of builders now fine-tune or customize on top of whatever they run. Almost nobody uses a model off the shelf. The moat is shifting from whose model you use to who controls the stack.

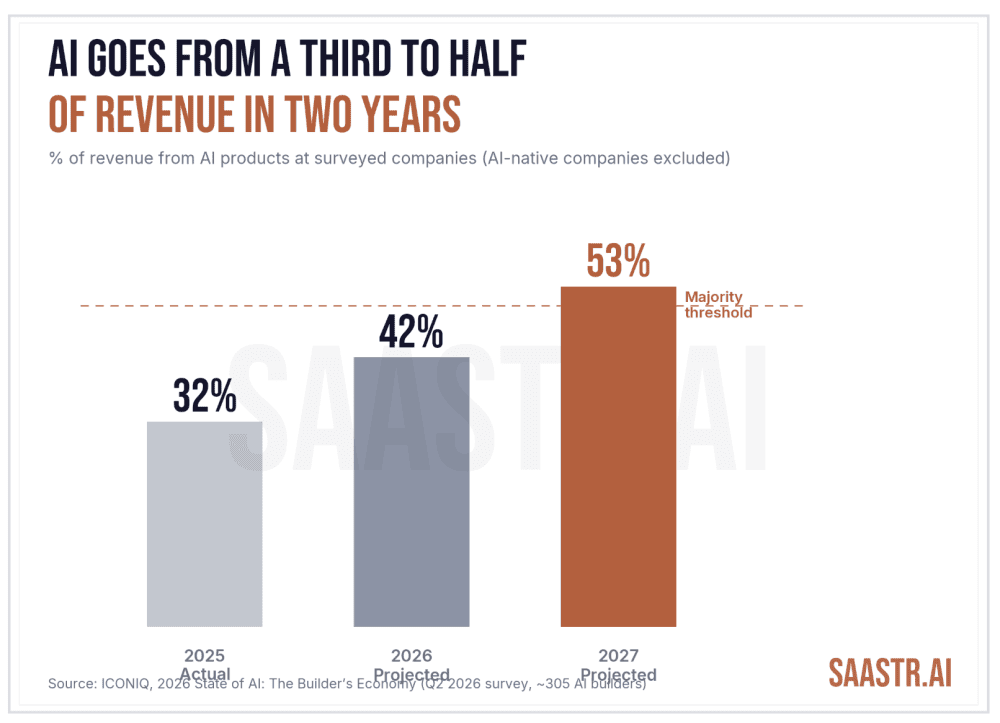

AI revenue trajectory: 32% to 42% to 53%

For companies that aren't AI-native (defined as 95%+ AI revenue), AI products went from 32% of revenue in 2025 to a projected 42% this year. ICONIQ projects 2027 crossing 53%, the majority threshold. In two years, AI goes from a third of the business to more than half.

That crossover is the whole premise of "The Builder's Economy." Once AI is the majority of revenue, it stops being an experiment line or a roadmap bet. It becomes what your margins, pricing, and valuation ride on. You resource it, staff it, and report it like the core business, because it is the core business.

One caveat: these are self-reported projections, and it's an unweighted average. A $10M shop that's 90% AI counts the same as a $2B company that's 10% AI. Read the arc as momentum, not market share.

Vertical apps dominate at 43%

Vertical AI applications are now the single most common product being built at 43%, well ahead of horizontal apps at 20% and consumer at 11%. Builders converged on the application layer, and inside it they're going deep into specific industries.

Financial services jumped to the #3 targeted use case from #8. Healthcare rose to #5 from #11. Customer support fell from #3 to #6. Teams are walking away from the easy, generic use cases and into hard, regulated domains where the workflow itself becomes the moat. Model-layer differentiation, by contrast, ranks dead last as a priority at 13%.

The use cases gaining fastest are the hardest and most regulated. Financial services and healthcare are climbing precisely because their workflow depth is what a general-purpose model can't copy overnight.

Agentic AI: top priority, weakest performer

Asked where they're investing in customer-facing product over the next 12 months, 66% put agentic AI capabilities in their top three. Clear leader. Agent reliability and orchestration infrastructure came next at 35%. The roadmap is pointed at agentic depth.

That's the ambition. The reality inside these same companies tells a different story. Internal agent productivity impact is stuck under 30% across every revenue band. Only 5% of teams say their agents rarely need human intervention. Nearly half report agents need a human occasionally, and another 39% need one frequently.

Agents are the top investment priority and the weakest performer at the same time. The bet is real. The payoff hasn't arrived.

AI gross margins: 45% to 53% to 59%

Average gross margin on AI products climbed from 45% in 2025 to a projected 53% this year, on track for 59% by 2027. That's 14 points of expansion in two years.

This number matters more than most people realize. Traditional SaaS gross margins run 70-80%. AI products started well below that because of inference costs. The gap is closing fast. If the 2027 projection holds, AI products will be margin-competitive with traditional software while delivering differentiated capabilities.

What the survey says about pricing and cost discipline

The margin expansion isn't accidental. The companies pulling ahead treat pricing, cost, and org design as product decisions. That's the recurring theme in ICONIQ's analysis. The operators who view these as afterthoughts are falling behind.

Jason Lemkin's summary of the report captures it: "The thesis moved in six months. The January edition was about proving AI works. This one is about proving AI pays." The shift from technical validation to commercial viability is complete at the top tier of companies. The rest are catching up.

Logicity's Take

The 58% fine-tuning number is the sleeper stat here. It means the winners aren't picking the best model, they're building the best system around whatever model they use. For SaaS founders, that shifts the build-vs-buy calculus. Tools like [n8n](https://logicity.in/r/n8n) for agent orchestration or [Airtable](https://logicity.in/r/airtable) as a data layer become more strategic than your LLM provider choice. The moat isn't the model. It's the pipeline, the prompts, and the integration layer. If you're treating your AI stack as a single vendor decision, you're already behind the 58%.

Disclosure

Some links in this post are affiliate links — Logicity earns a commission if you sign up, at no extra cost to you. We only link products we have used or actively recommend.

The methodology question

ICONIQ surveyed 305 executives at software companies building AI products. That's a self-selected group of AI builders, not a representative sample of all B2B software. The revenue projections are self-reported. The averages are unweighted by company size.

None of that makes the data wrong. It makes it a specific kind of data: the view from inside companies that are already committed to AI as a product strategy. If you're still debating whether to build AI features, this survey won't tell you what the median company looks like. It tells you what the builders are experiencing.

Frequently Asked Questions

What is the ICONIQ State of AI report?

A quarterly survey by ICONIQ Capital of software executives building AI products. The Q2 2026 edition surveyed 305 executives and focuses on commercial metrics rather than technical capabilities.

How much revenue do AI products generate at software companies?

Among surveyed companies (excluding AI-natives), AI products represent 42% of revenue in 2026, up from 32% in 2025, with projections of 53% by 2027.

What's the gross margin on AI products in 2026?

Average AI product gross margins reached 53% in 2026, up from 45% in 2025, with projections of 59% by 2027.

Are companies using open source or frontier AI models?

Both. Frontier APIs lead at 80% usage, but open source reached 40% and is growing faster. The average builder uses 3.3 providers and 58% fine-tune their models.

How reliable are AI agents in production?

Not very. Only 5% of teams report agents rarely need human intervention. Nearly half say agents need humans occasionally, and 39% need them frequently.

Related analysis on enterprise AI adoption challenges and security requirements.

Need Help Implementing This?

If you're building AI products and want to benchmark your metrics against ICONIQ's data, or need help with your AI pricing and margin strategy, reach out to Logicity's consulting team for a walkthrough.

Source: SaaStrAI

Huma Shazia

Senior AI & Tech Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.