Key Takeaways

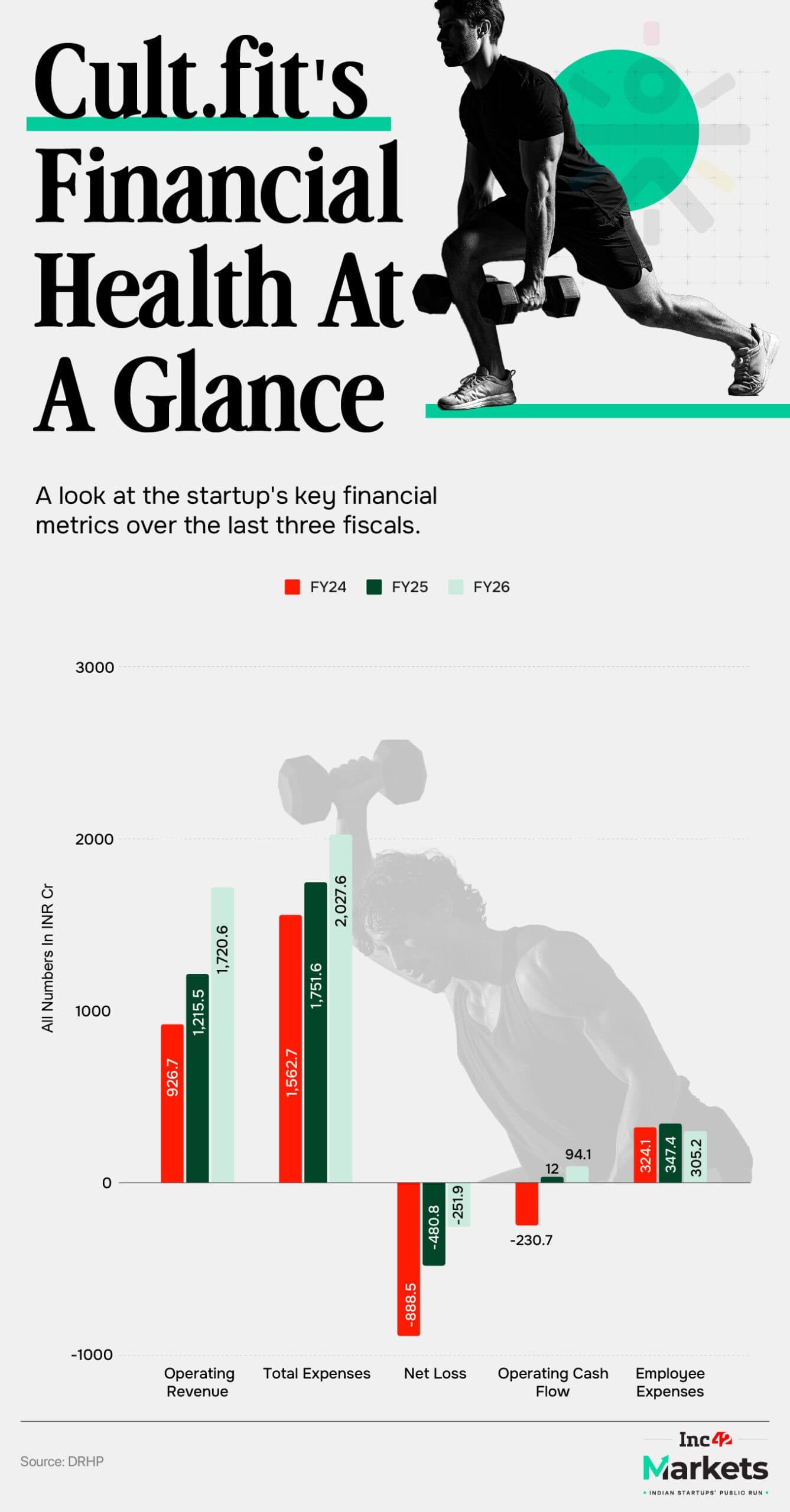

- Cult.fit cut net losses 48% to ₹251.9 Cr while growing revenue 41.6% to ₹1,720.6 Cr in FY26

- Operating cash flow surged from ₹12 Cr to ₹94 Cr, signaling genuine unit economics improvement

- Cultsport retail expansion targets 50 stores this year with ₹23.4 Cr allocated from IPO proceeds

Cult.fit's draft red herring prospectus tells a story the company has been trying to write for years: growth that actually pays for itself. The fitness startup posted ₹1,720.6 Cr in operating revenue for FY26, up 41.6% year-on-year, while cutting consolidated net losses nearly in half to ₹251.9 Cr from ₹480.6 Cr the previous year.

The more telling number sits in the cash flow statement. Operating cash flow jumped to roughly ₹94 Cr from approximately ₹12 Cr in FY25. For a business built on physical gyms, leases, and equipment, this shift from cash consumer to cash generator marks a structural change, not a cosmetic one.

Why is Cult.fit finally generating cash?

The company spent years building out infrastructure across India. Now it is harvesting returns from that investment rather than compounding it. Employee benefit expenses dropped to ₹305.2 Cr from ₹347.4 Cr despite stronger business growth. Operating expenses grew slower than revenue. These are the mechanics of operating leverage, and they appear in the numbers for the first time at meaningful scale.

CEO Naresh Krishnaswamy has described this shift publicly. After absorbing losses through heavy infrastructure investment, the company now prioritizes utilization at existing centers over aggressive expansion. Gym memberships continue growing from facilities already built.

This capital allocation discipline matters for the IPO thesis. According to Equentis Wealth Advisory Services, investors will assess Cult.fit's profitability roadmap and execution strategy rather than relying on brand recognition alone. The public market rewards operating leverage and clear pathways to profitability over raw top-line expansion.

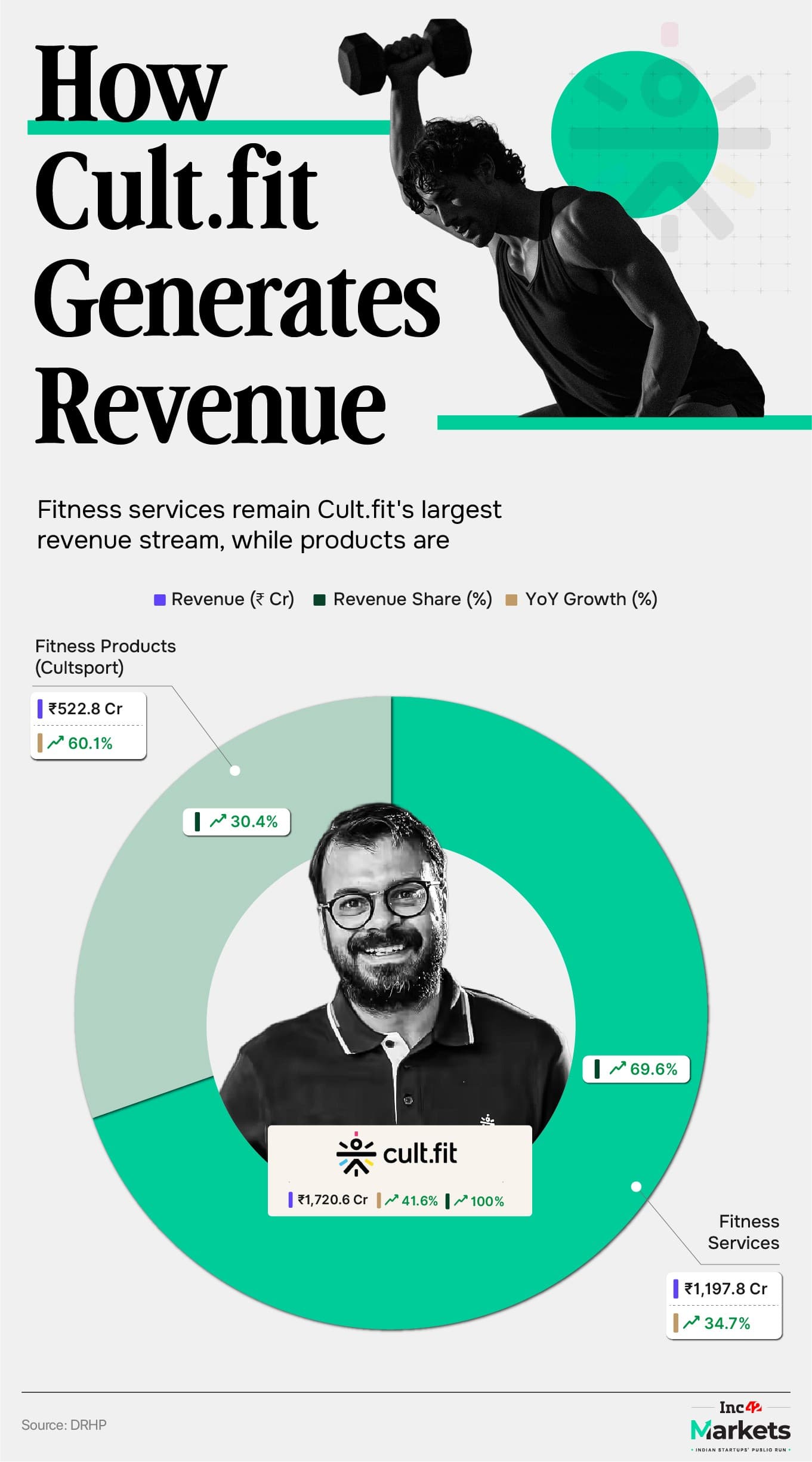

Cultsport becomes the second revenue engine

The DRHP reveals a structural shift beyond the core gym business. Cultsport, the company's sports accessories, apparel, footwear, and connected fitness devices arm, has been quietly scaling. Unlike fitness centers, these products generate incremental revenue without comparable infrastructure investment.

The economic profile differs sharply from the gym model. A customer acquired through fitness memberships can subsequently purchase equipment, apparel, or wellness products. The company monetizes the same user across multiple categories, increasing wallet share without proportional cost increases.

Cultsport's retail footprint is expanding. The brand currently operates 29 exclusive stores, with plans to reach 50 this year. The DRHP allocates ₹23.4 Cr toward store expansion. Until recently, Cultsport relied largely on digital commerce channels and third-party retailers. Dedicated stores allow customers to experience products before purchasing, a move toward controlled distribution.

Neoma Capital notes that scalable business models with improving unit economics command greater investor interest ahead of public listings. Cultsport fits that description better than the capital-intensive gym network.

What the IPO timing signals

Cult.fit is approaching public markets at a moment when Indian investors have grown skeptical of growth-at-all-costs narratives. The 2021 and 2022 vintages of consumer tech IPOs taught expensive lessons about valuations untethered from fundamentals. Companies now need to demonstrate that revenue growth converts to cash, not just investor presentations.

Cult.fit's FY26 numbers suggest the company understands this. The 48% loss reduction happened alongside 41.6% revenue growth. That combination indicates discipline, not just luck. Whether the company can sustain this trajectory through an IPO cycle and beyond remains the open question.

Risks that remain

The gym business still carries structural challenges. Customer acquisition costs in fitness remain high. Retention rates fluctuate seasonally. Physical infrastructure requires ongoing maintenance and lease obligations. Cult.fit's improving metrics show progress, not resolution of these inherent constraints.

Cultsport's retail expansion also introduces execution risk. Moving from online sales to exclusive stores requires different capabilities in real estate, inventory management, and in-store operations. The ₹23.4 Cr allocation for 21 additional stores will test whether the company can replicate early store economics at scale.

Logicity's Take

The Cult.fit IPO story is really two stories. The gym business demonstrates that operating leverage eventually kicks in for physical infrastructure plays, provided the company survives long enough to harvest it. Cultsport represents a hedge, a higher-margin, lower-capex business that can grow without proportional fixed cost increases. For finance teams watching Indian health-tech, the key metric to track post-IPO will be Cultsport's contribution margin relative to its share of revenue. If Cultsport scales faster than gym revenue while maintaining margins, Cult.fit's valuation thesis strengthens considerably. If it stalls, the company remains a gym chain with improving but still challenging unit economics.

Frequently Asked Questions

What is Cult.fit's revenue and loss position for FY26?

Cult.fit reported operating revenue of ₹1,720.6 Cr in FY26, up 41.6% year-on-year. Net losses fell 48% to ₹251.9 Cr from ₹480.6 Cr in FY25.

How much funding has Cult.fit raised before the IPO?

Cult.fit has raised over $660 million in funding from investors including Accel, Kalaari Capital, Zomato, and Tata Digital. The company reached a peak valuation of $1.5 billion during 2021 funding rounds.

What is Cultsport and how does it differ from Cult.fit gyms?

Cultsport is Cult.fit's sports accessories, apparel, footwear, and connected fitness devices business. Unlike gyms, it generates revenue without heavy infrastructure investment and is expanding to 50 retail stores from 29 currently.

How much is Cult.fit allocating for Cultsport store expansion?

The DRHP allocates ₹23.4 Cr toward Cultsport retail store expansion, targeting 50 stores this year.

What does Cult.fit's operating cash flow improvement indicate?

Operating cash flow rose from approximately ₹12 Cr in FY25 to nearly ₹94 Cr in FY26, indicating the business now generates cash from operations rather than consuming it, a critical shift for IPO readiness.

Relevant context on how startups approach revenue metrics and transparency ahead of funding or IPO milestones.

Need Help Implementing This?

If your finance team is tracking Indian startup IPOs or building investment thesis frameworks for health-tech companies, reach out to Logicity for analysis templates and sector benchmarking tools.

Source: Inc42 Media / Debarghya Sil

Manaal Khan

Tech & Innovation Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.