Key Takeaways

- Mega deals fell 55% YoY to just 5 rounds exceeding $100M in H1 2026

- Late-stage funding dropped 29% to $2.2 billion as investors prioritize profitability over growth

- Delayed IPOs from Flipkart, PhonePe, and others are disrupting the VC liquidity cycle

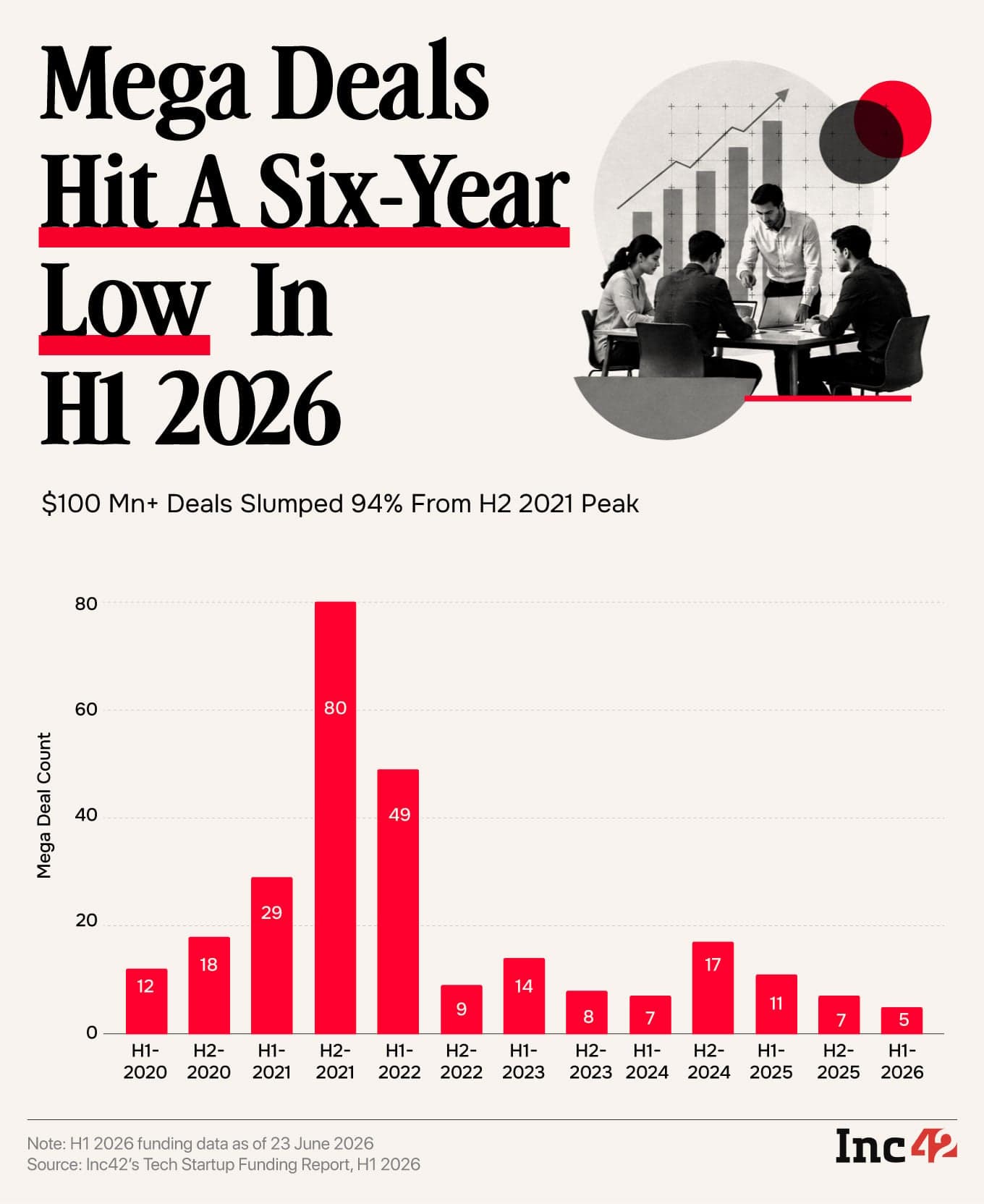

Indian mega deals, funding rounds exceeding $100 million, fell 55% in the first half of 2026. Only five startups cleared that threshold: CRED, Rapido, Spinny, Sarvam, and KreditBee. A year earlier, 11 companies raised rounds that large.

The numbers come from Inc42's Indian Tech Startup Funding Report for H1 2026. Overall late-stage funding dropped 29% year-over-year to $2.2 billion, and median ticket size collapsed 68% to $10 million. Early and growth-stage rounds, by contrast, rose 18% and 15% respectively. The pullback is concentrated at the top of the funnel.

Why are late-stage investors pulling back?

The short answer: discipline. Mansi Aggarwal, partner at Alkemi Growth Capital, told Inc42 that investor sentiment has shifted from a growth-first mindset to one prioritizing revenue quality, visibility into profitability, and governance. The days of funding growth at any cost are over.

Governance failures over the past few years accelerated this shift. Founders misrepresenting financials, startups raising round after round without demonstrating sustainable fundamentals. These cases made late-stage investors far more cautious about writing nine-figure checks.

Sudhir Rao, managing partner at Celesta Capital, offered a different lens: timing. Late-stage funds typically hold investments for five to eight years. H2 2021 marked the peak of India's funding boom, with 80 mega deals. Many investors who deployed capital then are now past their typical holding period.

“We have to look at what the typical holding period of late stage ownership has been. If that period is being crossed, investors are now looking for either an M&A event or an IPO. So one reason could simply be that we're in a stall phase of the cycle.”

— Sudhir Rao, Managing Partner at Celesta Capital

The pipeline problem

Mega deals depend on companies graduating from Series B and C rounds. If growth-stage startups stall, the pool of candidates for $100M+ rounds shrinks. Rao pointed to this pipeline effect as a compounding factor.

Geopolitical instability and macroeconomic pressure weighed on Q1 2026 and persisted through Q2. These external factors made both founders and investors more conservative. Startups that might have pushed for aggressive expansion chose to extend their runways instead.

Delayed IPOs are disrupting the liquidity cycle

Several large startups, including Flipkart, PhonePe, Curefoods, and Captain Fresh, deferred their IPO plans in H1 2026. Volatility in Indian equity markets and valuation concerns drove the delays.

This creates a knock-on effect for the entire ecosystem. IPOs are the preferred exit for late-stage investors. When listings get pushed back, liquidity events stall. Investors sitting on unrealized gains have less capital to redeploy into new mega rounds. The cycle slows.

M&A activity, the other major exit route, has also declined. With both channels constrained, late-stage capital is locked up rather than recycled into new investments.

Early-stage funding tells a different story

The contrast with earlier stages is striking. Seed and Series A activity rose, suggesting that investor appetite for Indian startups remains strong, just at different check sizes and risk profiles.

This bifurcation makes sense. Early-stage bets are smaller and spread across more companies. Late-stage investors face higher stakes and demand clearer evidence of sustainable business models before committing. The bar has simply risen.

Logicity's Take

For fintech and finance teams, this funding environment has practical implications. Late-stage capital scarcity means startups will stretch their runways, which often translates to slower hiring and more cautious vendor spending. If you're selling to startups, expect longer sales cycles and more scrutiny on ROI. If you're at a startup, the mandate is clear: prove unit economics before your Series C pitch. The growth-at-all-costs playbook is closed for the foreseeable future.

What happens next?

The second half of 2026 depends largely on whether IPO windows reopen. If Flipkart or PhonePe list successfully, the resulting liquidity could unlock capital for new late-stage investments. But if market volatility persists, the drought extends.

Rao's framing is useful here: this may simply be a stall phase. Funding markets move in cycles. The 2021 peak was an anomaly, and the current correction brings late-stage activity closer to historical norms. That's cold comfort for startups needing to raise, but it's not a structural collapse.

Another view on how AI startups are navigating valuation pressures in the current funding climate

Frequently Asked Questions

How many mega deals happened in India in H1 2026?

Five startups raised rounds exceeding $100 million: CRED, Rapido, Spinny, Sarvam, and KreditBee. This represents a 55% decline from the 11 mega deals recorded in H1 2025.

Why is late-stage funding declining in India?

Three main factors: investors prioritizing profitability over growth, the natural maturation of fund holding periods from the 2021 boom, and delayed IPOs that are locking up capital that would otherwise be recycled into new investments.

Is early-stage funding also declining in India?

No. Early-stage and growth-stage funding both increased in H1 2026, up 18% and 15% respectively. The pullback is concentrated in late-stage rounds.

Which Indian startups delayed their IPOs in 2026?

Flipkart, PhonePe, Curefoods, and Captain Fresh all deferred listing plans amid equity market volatility and valuation concerns.

Need Help Implementing This?

Logicity helps fintech and finance teams navigate funding cycles with actionable intelligence. Subscribe to our newsletter for weekly analysis on startup funding, M&A activity, and market trends that affect your business.

Source: Inc42 Media / Palak Sharma

Huma Shazia

Senior AI & Tech Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.