Key Takeaways

- 44 million Americans (17% of adults) are subprime consumers, a stable segment tracked across 47 monthly surveys

- Young subprime consumers face acute healthcare pressure: 23% delayed doctor visits, 38% borrowed from family for medical costs

- BNPL usage among subprime consumers hit 19%, above the 13% sample-wide rate, signaling appetite for flexible payment tools

Forty-four million Americans carry subprime credit, and they are not going anywhere. A PYMNTS Intelligence report released this week confirms that subprime consumers represent 17% of U.S. adults, a share that has held steady between 14% and 23% across 47 monthly survey waves. This is not a temporary population stressed by macro conditions. It is a permanent market segment, one increasingly served by buy now, pay later (BNPL) providers, healthcare financing startups, and card issuers willing to build products around irregular cash flow.

Healthcare is the pressure point

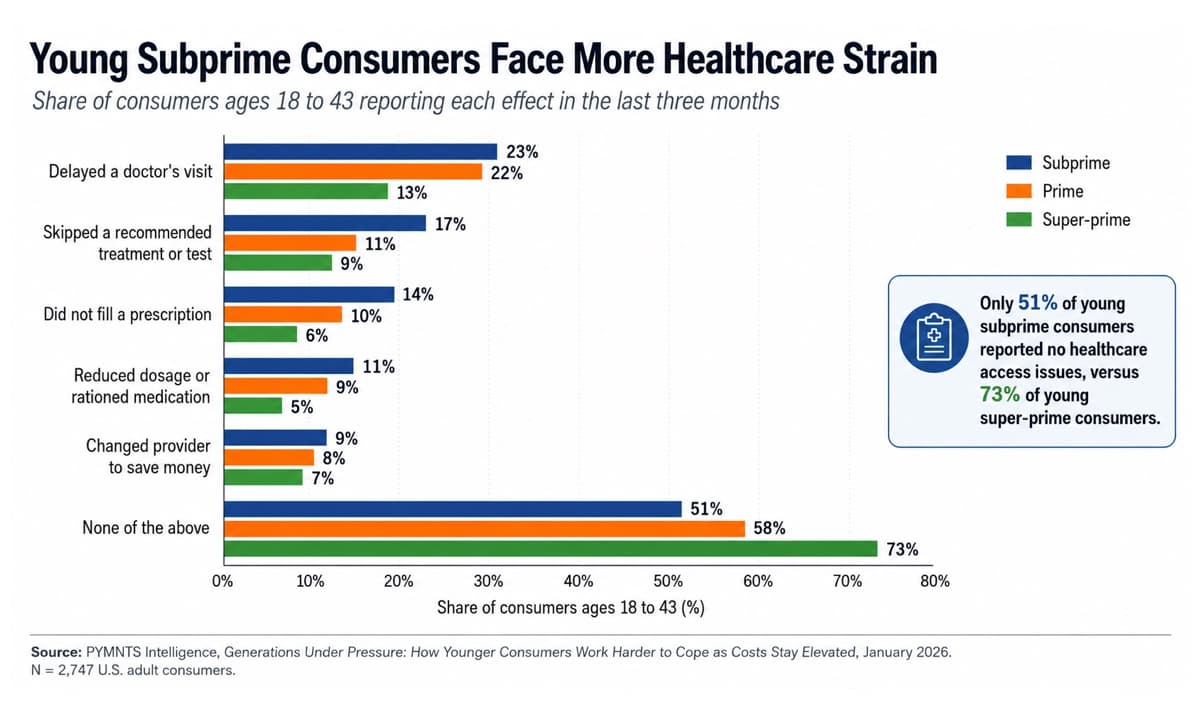

The report's most striking data concerns medical costs. Only 51% of young subprime consumers (ages 18 to 43) reported no healthcare access issues. Compare that to 58% of young prime consumers and 73% of young super-prime consumers. The gap translates into real decisions: 23% delayed a doctor's visit, 17% skipped a recommended treatment or test, 14% did not fill a prescription, and 11% rationed medication.

To cover these costs, 38% of young subprime consumers borrowed from family or friends. Another 31% negotiated bills or set up payment plans directly with providers. And 26% used BNPL or installment financing at the healthcare checkout. These are not edge cases. They represent the dominant payment strategies for a population locked out of traditional credit lines.

Credit cards are absent; BNPL fills the gap

Thirty-five percent of subprime consumers hold no credit or store card at all. For prime consumers, that figure drops to 12%. For super-prime, it is 4%. The card market has, in effect, abandoned a third of subprime borrowers.

BNPL providers have moved in. Subprime BNPL usage runs at 19%, well above the 13% sample-wide average. The appeal is obvious: approval happens at checkout, installments are fixed, and the decision is made in the moment when the consumer knows exactly what they need to buy.

There is a positive signal buried in the data. The share of subprime consumers who always or usually revolve credit card balances dropped from roughly 50% in mid-2023 to 38% in January 2026. That decline suggests either better payment discipline or a migration away from cards entirely, both outcomes that reduce reliance on high-interest revolving debt.

Tax refunds act as working capital

Among subprime tax refund recipients, 67% said their refund was critical or very important to their finances. The whole-sample figure is 48%. For many subprime households, the annual refund functions less like a windfall and more like a bridge loan in reverse, a lump sum that covers accumulated gaps from the prior year and pre-funds the next few months of obligations.

This seasonality matters for payments providers. Subprime consumers are not static risk profiles. Their cash flow swings predictably around tax season, paydays, and benefit cycles. Products that flex with those rhythms, offering smaller payments during lean weeks and larger ones when funds arrive, can reduce defaults while serving real needs.

What this means for fintech product teams

The report reframes subprime consumers as active financial managers, not passive high-risk borrowers. They toggle between credit cards, BNPL, informal loans from family, and provider payment plans depending on the expense and the week. Each tool fills a gap until the next paycheck or refund arrives.

Healthcare finance is the clearest whitespace. Young subprime consumers are already signaling demand at the doctor's office, pharmacy counter, and telehealth checkout. Providers like Walnut, PayZen, and Affirm's healthcare verticals are building here, but the market remains fragmented. Card networks and issuing banks have largely stayed on the sidelines, ceding ground to point-of-sale lenders.

Timing and transparency matter more than credit limits. A subprime consumer who can see exactly when each payment is due, and adjust it around paydays, is less likely to default than one given a revolving line with opaque minimums. The BNPL model's success among this group is partly about approval rates, but also about predictability.

Logicity's Take

The 44-million figure is a floor, not a ceiling. As medical debt grows and card issuers tighten underwriting, more consumers will functionally behave like subprime borrowers even if their scores stay higher. For fintech teams, the opportunity is in vertical-specific products: healthcare financing with provider integrations, payroll-linked repayment for gig workers, and refund-advance products that compete with predatory tax-prep loans. The winners will be those who treat subprime not as a risk bucket but as a product-design constraint. The data is clear: this population is already managing complexity. The question is whether financial products will help or add friction.

Frequently asked questions

Frequently Asked Questions

How many subprime consumers are in the US?

PYMNTS Intelligence counts 44 million subprime adults, representing 17% of the US consumer population. That share has remained between 14% and 23% across 47 monthly surveys.

Why do subprime consumers use BNPL more than others?

Thirty-five percent of subprime consumers hold no credit card, limiting their payment options. BNPL offers instant approval at checkout with fixed installments, making it accessible where traditional credit is not.

What healthcare issues do young subprime consumers face?

Among young subprime consumers, 23% delayed doctor visits, 17% skipped treatments, 14% did not fill prescriptions, and 11% rationed medication. Only 51% reported no healthcare access issues.

Are subprime consumers improving their credit habits?

The share who always or usually revolve credit card balances dropped from about 50% in mid-2023 to 38% in January 2026, suggesting either better discipline or reduced card reliance.

Another look at financing strategies under credit constraints

Need Help Implementing This?

Logicity advises fintech and payments teams on product strategy, underwriting design, and market sizing for underserved segments. Reach out at hello@logicity.in to discuss your roadmap.

Source: PYMNTS | / PYMNTS

Manaal Khan

Tech & Innovation Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.