Key Takeaways

- Zoom revenue grew 5.5% YoY to $1.24B quarterly, re-accelerating after hitting a 3% floor

- AI Companion paid users jumped 184% YoY, proving AI monetization is possible at enterprise scale

- Enterprise now drives 61% of revenue while self-serve growth lags at 2.8%

Zoom posted $1.239 billion in Q1 FY2027 revenue, up 5.5% year-over-year, beating guidance and marking its clearest re-acceleration since the post-pandemic slowdown. The company everyone dismissed as a COVID one-hit wonder now trades at a $27 billion market cap, generates 40% free cash flow margins, and is actually charging customers for AI. That last part matters most for SaaS operators watching the AI revenue question unfold.

The numbers tell a story of a mature B2B company that found its footing. Revenue run-rate sits around $5 billion with FY27 guidance of $5.08 billion. Non-GAAP operating margin came in at 41.1%. Free cash flow hit $500 million in the quarter alone. And Zoom's Anthropic stake, carried at $1.27 billion on the books, is likely worth $2 to $4 billion at current AI valuations. That's a 25x return on what started as a strategic bet.

How did Zoom restart growth at $5 billion scale?

Zoom fell to roughly 3% growth after the pandemic surge faded. The narrative was set: Teams would eat its lunch, offices would reopen, and the stock would slowly bleed. Some of that happened. But growth has now climbed for multiple consecutive quarters, and full-year FY26 growth accelerated 130 basis points to 4.4%.

The pattern here is instructive. At scale, growth doesn't die. It plateaus. And a plateau can be climbed back out of if you attach genuinely new products to a large installed base. The installed base is the asset. The second and third products are the growth. Zoom's Contact Center and AI Companion are those products.

Is Zoom actually making money from AI?

Yes. AI Companion paid users grew 184% year-over-year. The company's "My Notes" feature reached 1.5 million licensed users within four months of launch. Customer Experience revenue is growing at high double digits, and paid AI showed up in every one of Zoom's top 10 CX deals last quarter.

The difference: Zoom built AI into paid SKUs and customers are buying them. Charging for AI instead of giving it away is a completely different financial outcome. Shipping AI features is table stakes now. Getting customers to pay for them is the actual skill. Many SaaS companies are still figuring out where AI sits in their pricing, bundling it free to drive adoption. Zoom picked the other path and it's working.

Enterprise now carries the company

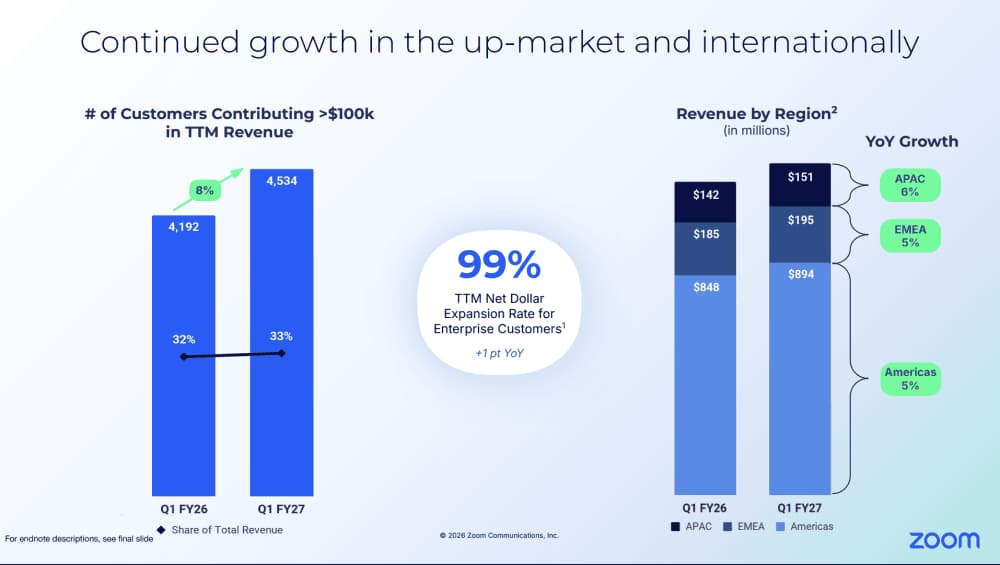

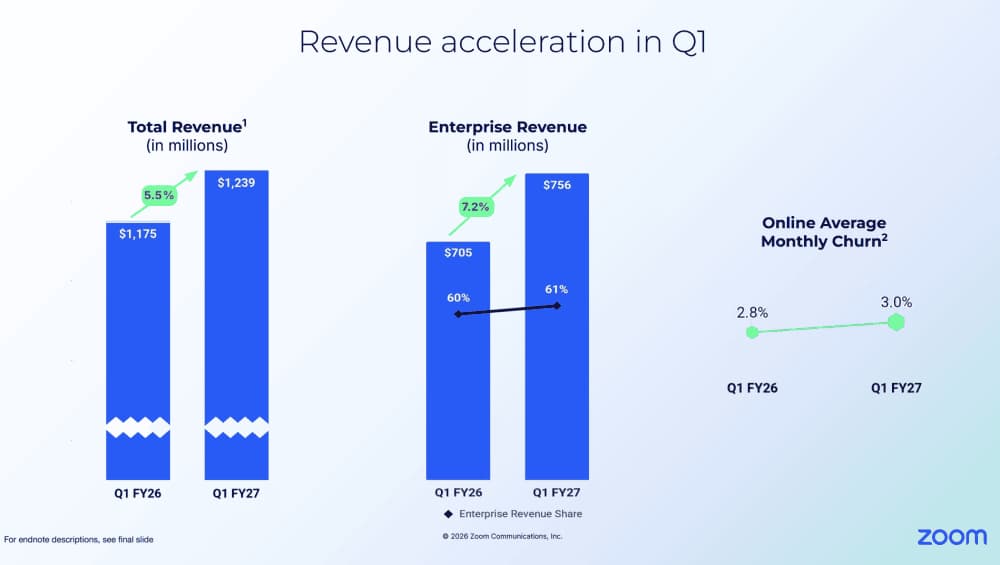

Enterprise revenue hit $755.7 million, up 7.2%, and now makes up 61% of total revenue. Online self-serve revenue was $483.3 million, up just 2.8%. The thing that made Zoom explode, millions of people swiping credit cards during lockdowns, is now the slow-growth anchor growing at a third of the enterprise rate.

This isn't new, but the acceleration continues. Customers spending $100k or more grew 8.2% to 4,534 accounts. The direct, sales-led enterprise motion is the engine keeping the whole thing moving. Self-serve got Zoom to massive scale but couldn't sustain growth on its own.

The lesson for SaaS founders: if your self-serve base is decelerating, the fix is usually enterprise and multi-product. Pouring more into the top of the self-serve funnel often yields diminishing returns at scale.

Net revenue retention is still below 100%

Enterprise net dollar expansion ticked up to 99%, from 98% a year ago. Still under 100%. Online average monthly churn actually got worse, rising to 3.0% from 2.8%. Growth is being driven by new logos and new product attach, not by the existing base expanding on its own.

You don't strictly need 120% NDR to grow. You can grow with sub-100% retention if you add enough new customers and attach enough new products. But it's much harder, and it's lower-quality growth. Most great B2B companies would kill for Zoom's cash flow. Zoom, in turn, would love to get NDR back well over 100%.

The cash machine metrics

Zoom generated $500 million in free cash flow on a 40.4% FCF margin. Combined with operating margin of 41.1%, the Rule of 40 score sits at roughly 46. Cash and marketable securities total $7.7 billion. Back out that cash from the $27 billion market cap and you get an enterprise value of about $19 billion, or roughly 4x revenue.

For a company growing at 5%, that multiple looks fair. For a company that's re-accelerating with real AI attach, generating 40% FCF margins, and sitting on a multi-billion-dollar Anthropic stake, the market might be underpricing optionality.

Logicity's Take

Zoom's playbook is the clearest proof that AI monetization at enterprise scale is real, not theoretical. The 184% growth in AI Companion paid users matters more than any feature announcement. SaaS founders watching the "do we charge for AI or bundle it free" debate should note that Zoom chose to charge, built AI into distinct SKUs, and customers said yes. The harder lesson: Zoom's sub-100% NRR means even with AI attach working, the base still contracts. If you're building a product-led motion expecting it to carry you forever, Zoom is the $5 billion case study showing it won't. Enterprise and multi-product expansion become the only durable growth path past a certain scale.

Frequently Asked Questions

What is Zoom's current ARR?

Zoom's revenue run-rate is approximately $5 billion, with full-year FY27 guidance of $5.08 billion based on Q1 FY2027 quarterly revenue of $1.239 billion.

How fast is Zoom growing in 2026?

Zoom's Q1 FY2027 revenue grew 5.5% year-over-year, re-accelerating from a low of roughly 3% growth. Enterprise revenue specifically grew 7.2%.

Is Zoom profitable?

Yes. Zoom reported 41.1% non-GAAP operating margin and 40.4% free cash flow margin, generating $500 million in FCF in Q1 alone. The company holds $7.7 billion in cash and investments.

How is Zoom monetizing AI?

Zoom built AI Companion into paid SKUs rather than offering it free. Paid AI users grew 184% YoY, and AI features appeared in every top 10 Customer Experience deal last quarter.

What is Zoom's Anthropic investment worth?

Zoom carries its Anthropic stake at $1.27 billion on the books, but current AI valuations suggest it could be worth $2 to $4 billion, representing approximately a 25x return.

Need Help Implementing This?

If you're building a SaaS company navigating the self-serve to enterprise transition or figuring out AI monetization, Logicity covers the strategies that actually work. Subscribe for weekly breakdowns of what leading B2B companies are doing differently.

Source: SaaStrAI

Manaal Khan

Tech & Innovation Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.