Key Takeaways

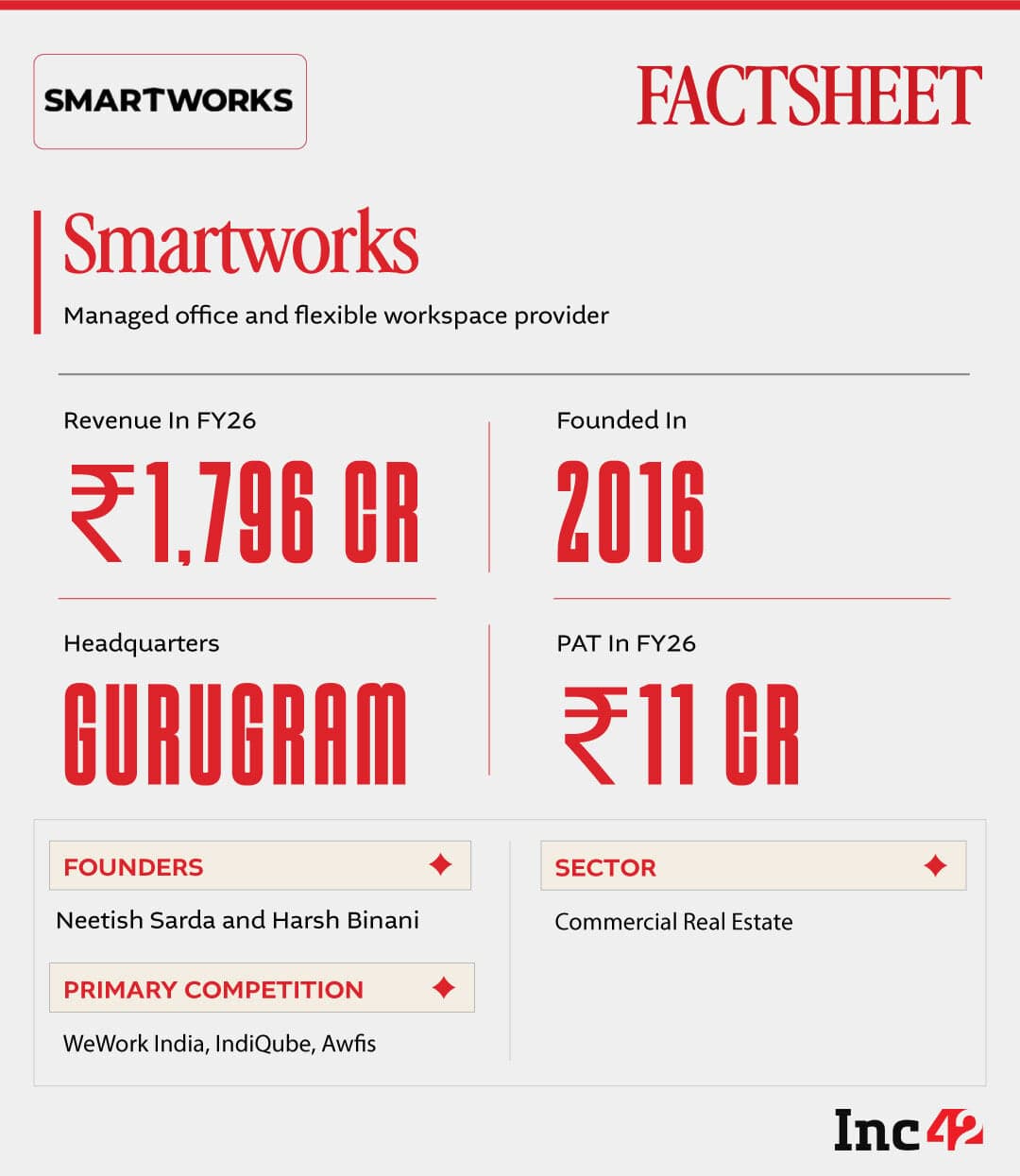

- 90% of Smartworks' revenue now comes from enterprise clients, with 37% from companies taking 1,000+ seats

- India's flex workspace stock is projected to reach 140-145 Mn sq ft by FY28, driven heavily by GCC demand

- Smartworks delivers operational offices in 45-60 days versus 9-12 months for traditional leases

Smartworks derives 90% of its revenue from enterprise clients, a stark contrast to the startup-heavy customer base that defines most Indian coworking operators. The company's founder Neetish Sarda calls this positioning a contrarian bet. When Smartworks launched, the flex workspace market was synonymous with freelancers and bean-bag offices. Large corporations leased their own buildings.

That calculus has shifted. India's flexible workspace capacity is projected to reach 140-145 million square feet by FY28, according to CRISIL. The primary driver is not startups but Global Capability Centers. GCCs are expected to become a $105 billion industry by 2030, and they need office space that scales fast across multiple cities.

Why did Smartworks avoid the startup market?

Sarda's thesis was simple: the real margin was in serving large enterprises, not renting desks to small teams. Traditional leasing required companies to lock capital for years, invest in fit-outs, and wait nine to 12 months before moving in. For a multinational opening offices in Bangalore, Hyderabad, and Pune simultaneously, that model created bottlenecks.

Smartworks approached the problem like a cloud computing provider. "Our view was that workspaces would evolve like cloud computing – companies would consume office infrastructure as a service, rather than owning it," Sarda told Inc42. The company leases entire buildings or large campuses, then integrates technology, security, collaboration zones, and wellness facilities into a standardized product.

The result is what Smartworks calls a 'Managed Office Campus.' These spaces can go operational in 45-60 days. Enterprises can start with a few hundred seats and expand to thousands without relocating.

How did enterprises respond to the pitch?

Skeptically, at first. Convincing Fortune 500 companies to move 1,000+ employees into a managed workspace required proving reliability, security, and execution speed. Investors and landlords were equally doubtful. The idea that large corporations would abandon traditional leases seemed far-fetched in 2016.

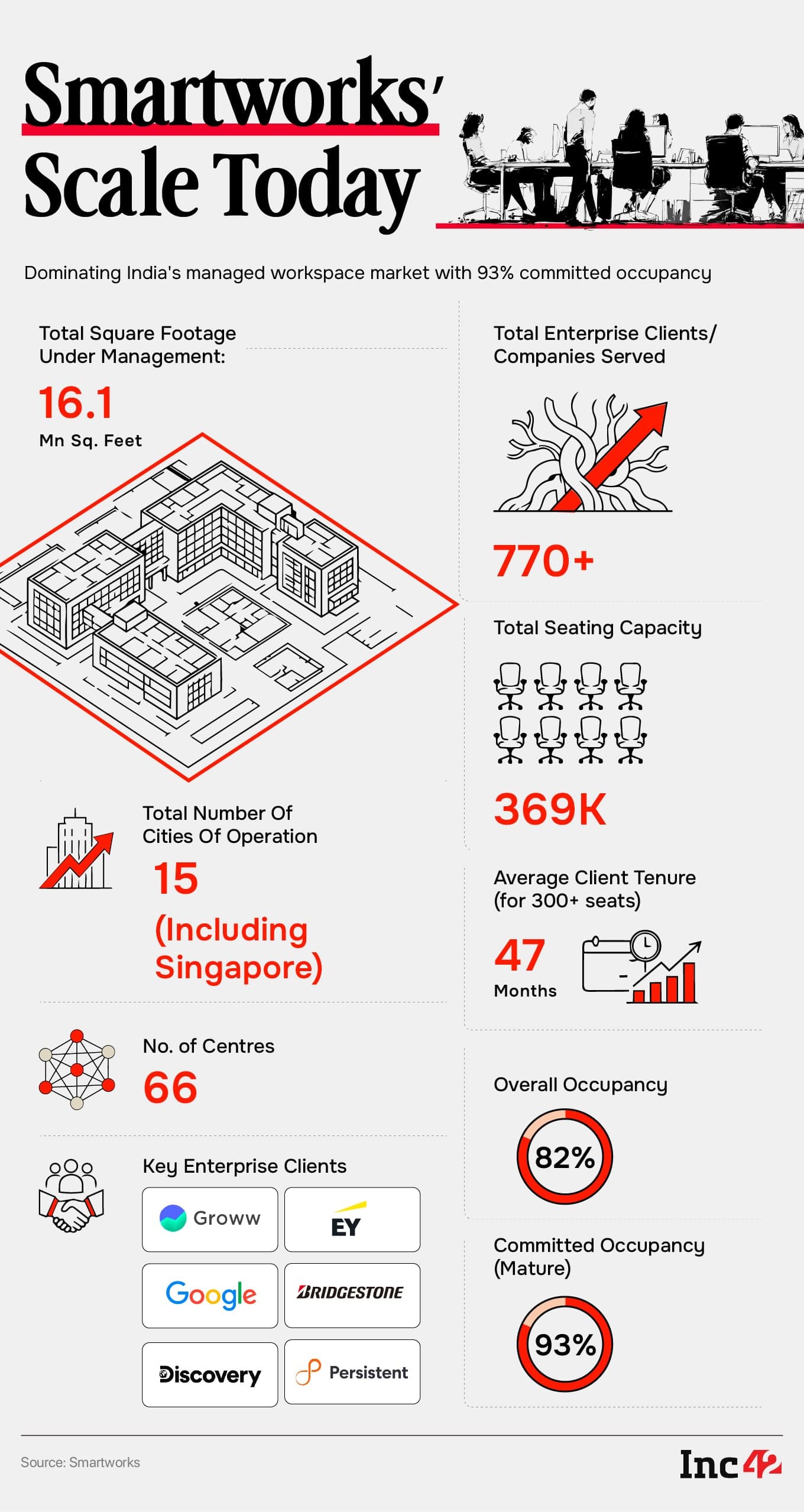

Execution changed minds. Early clients saw functional campuses delivered within weeks, complete with enterprise-grade infrastructure. Individual deployments expanded into multi-city rollouts. Smartworks adopted a cluster-based expansion strategy, deepening presence in key business hubs rather than spreading thin. Today, the company operates 66 centers across 15 cities, including Singapore.

What makes GCCs a critical growth driver?

India hosts over 1,700 GCCs. These are not small operations. Companies like Google, Microsoft, JPMorgan, and Walmart run engineering centers, analytics hubs, and operational units from Indian cities. They need campus-style environments that reflect global brand standards while scaling rapidly.

GCCs are projected to drive demand for 160-200 million square feet of office space by 2030. Flex workspaces could capture nearly half. For a GCC opening simultaneously in three cities, the traditional lease model creates 9-12 month delays per location. A managed workspace provider that delivers in 60 days solves a real procurement problem.

How does Smartworks compare to competitors?

Competition has intensified. Awfis, backed by Blackstone, went public in 2024 and operates a network of smaller centers across more cities. IndiQube focuses on mid-market enterprises with a build-to-suit model. WeWork India, after restructuring its global parent's issues, remains active in premium urban locations.

Smartworks differentiates on scale. The company claims to hold over 10% of India's flex workspace stock, the largest share in the segment. Its focus on large-format campuses means fewer but bigger deals. That creates dependence on complex, lengthy sales cycles but produces more predictable recurring revenue once contracts close.

The trade-off is visible in growth patterns. Competitors chasing startups and SMBs scaled seat counts faster in early years. Smartworks grew slower but built a client base less sensitive to economic downturns. Enterprises on multi-year contracts do not churn as quickly as small teams that outgrow a 10-seat office.

What are the risks in the enterprise-first model?

Client concentration is the obvious one. When 37% of revenue comes from large accounts, losing one or two major clients hits hard. Long sales cycles mean revenue visibility lags behind occupancy commitments. Smartworks must often commit to multi-year building leases before securing anchor tenants.

GCC demand, while growing, is sensitive to global corporate budgets. If a U.S. tech company slows hiring, its Hyderabad GCC does not need additional seats. The 2022-2023 tech slowdown demonstrated this. Flex workspace absorption dipped before recovering in 2024.

Logicity's Take

For finance teams evaluating real estate OpEx, Smartworks represents a shift from capital expenditure to operating expense. Traditional leases require 15-25% of total setup cost as upfront fit-out investment. Managed workspaces convert that to a monthly seat cost, improving cash flow predictability. Competitors like Awfis (INR 8,000-15,000/seat/month for standard plans) and WeWork India (premium tier at INR 18,000-25,000/seat/month) offer different price-to-amenity ratios. CFOs should model total occupancy cost over a 3-year horizon, including hidden costs like maintenance, security, and technology refresh that managed workspace contracts bundle in.

Frequently Asked Questions

How fast can Smartworks deliver a functional office?

Smartworks claims 45-60 days from contract to operational workspace, compared to 9-12 months for traditional lease and fit-out cycles.

What percentage of Smartworks revenue comes from enterprises?

90% of Smartworks' revenue comes from enterprise clients, with 37% from companies occupying 1,000+ seats.

How large is India's flexible workspace market projected to grow?

CRISIL projects India's flex workspace stock to reach 140-145 million square feet by FY28.

Why are GCCs driving demand for managed workspaces?

GCCs need rapid multi-city office setups without 5-7 year lease commitments. The segment is projected to drive demand for 160-200 million sq ft by 2030.

Enterprise infrastructure decisions, whether workspace or AI governance, share similar CFO-level evaluation criteria

Need Help Implementing This?

Evaluating managed workspace providers for your GCC or enterprise expansion? Logicity can connect you with real estate consultants and finance advisors who specialize in flex space contracts. Contact our team for introductions.

Source: Inc42 Media / Inc42 BrandLabs

Huma Shazia

Senior AI & Tech Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.