Key Takeaways

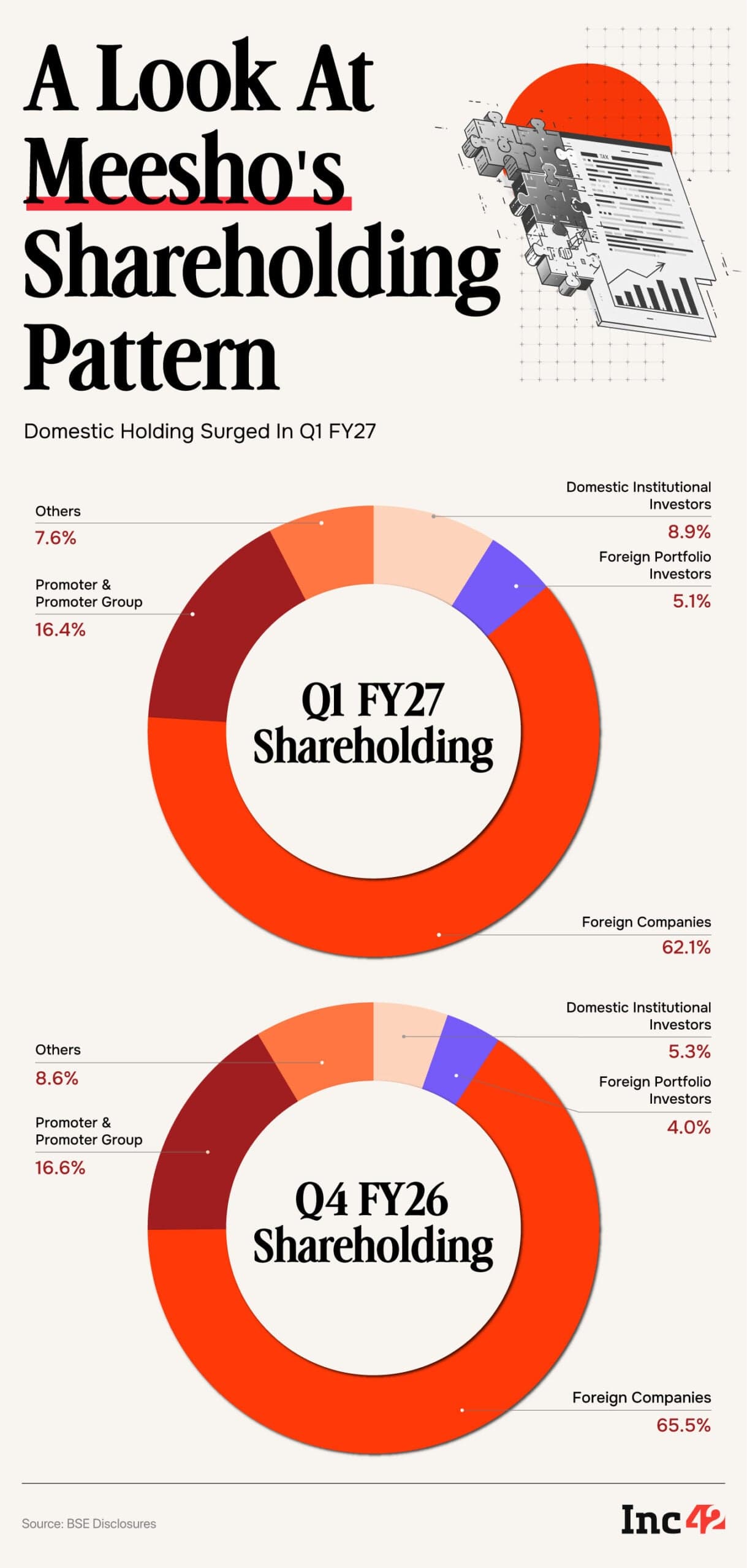

- Mutual funds bought 15.18 Cr additional Meesho shares in Q1 FY27, raising collective stake to 7.93%

- Foreign company holdings dropped from 65.51% to 62.05% after the June 9 lock-in expiry

- SBI Mutual Fund now holds the largest domestic institutional stake at 3.01%

Indian mutual funds scooped up over 15 Cr Meesho shares in the June quarter as early foreign investors headed for the exits. Domestic ownership in the ecommerce company jumped to 8.89% from 5.55% three months earlier, while foreign company holdings slid to 62.05% of diluted share capital. The trigger: Meesho's post-IPO lock-in expired on June 9, freeing roughly 68% of outstanding equity for trading.

Who sold and who bought?

Fidelity moved first. The day after the lock-in expired, FID FDI 2117 LLC and FID FDI 312 LLC offloaded 5.98 Cr shares through bulk deals. Astrend India followed with another 1.06 Cr shares. In total, 17 foreign companies exited Meesho's cap table entirely, cutting the number of such investors from 67 to 50.

The marquee names stayed put. Peak XV Partners, SoftBank, Prosus, Elevation Capital, and RPS Ventures held their positions. But smaller foreign shareholders collectively sold 16.68 Cr shares during the quarter.

Domestic institutions absorbed nearly all of it. Twenty-seven mutual funds now hold a combined 7.93% stake, up from 4.72% held by 23 schemes in March. SBI Mutual Fund emerged as the largest domestic institutional shareholder with 3.01%. Invesco India and Aditya Birla Sun Life each crossed the 1% threshold.

Why are AIFs joining the buying?

Alternative investment funds also increased exposure. Holdings rose to 3.74 Cr shares across 29 AIFs, up from 2.59 Cr shares held by 18 funds in the previous quarter. The breadth matters: more funds entering signals growing institutional conviction rather than a concentrated bet by one or two players.

In absolute numbers, domestic shareholders owned 42.13 Cr shares at the end of June, up from 25.35 Cr shares three months earlier. That's a 66% increase in domestic holdings within a single quarter.

A pattern emerging across Indian tech listings

Meesho's ownership shift mirrors what happened at Paytm. The fintech company, public since 2021, saw domestic shareholding cross 50% this year after foreign investors reduced their stake to 49.4% in the March quarter. Domestic investors continued buying through the June quarter.

The dynamic is predictable. Venture capital funds face pressure to return capital to their LPs. Once lock-ins expire, they book profits. Indian mutual funds and AIFs, flush with inflows and mandated to deploy domestically, step in as natural buyers.

For listed new-age tech companies, higher domestic ownership typically means lower volatility. Foreign institutional investors react faster to global risk-off events. Local institutions, especially mutual funds with SIP inflows, tend to hold through drawdowns.

What does the price action say?

Meesho shares closed 1.9% lower at ₹185.60 on the day the shareholding data emerged. The stock remains volatile. But the selling pressure from foreign exits has been absorbed without a collapse, suggesting adequate demand from domestic buyers.

The real test comes if another large foreign holder decides to exit. SoftBank, Prosus, and Peak XV collectively hold substantial positions. Any bulk sale by these investors would test whether domestic demand can scale further.

Logicity's Take

The Meesho ownership transition is a liquidity event, not a vote of no-confidence. Early-stage VCs exiting after lock-up is standard playbook. What's notable is the speed at which domestic institutions absorbed the selling. SBI MF's 3.01% stake signals that large domestic asset managers view Meesho as a core India consumption bet. For fintech teams tracking public market benchmarks: the social commerce segment now has a cleaner shareholder base, which typically supports higher valuation multiples once profitability metrics improve.

Frequently Asked Questions

Why did foreign investors sell Meesho shares after the lock-in expired?

Post-IPO lock-ins prevent early investors from selling immediately. Once the lock-in ends, VCs often sell to return capital to their limited partners. Fidelity and 16 other foreign entities exited or reduced positions in Meesho's June quarter.

Which mutual funds hold the largest Meesho stakes?

SBI Mutual Fund leads with 3.01%. Invesco India Mutual Fund and Aditya Birla Sun Life Mutual Fund each hold more than 1%. Twenty-seven funds collectively own 7.93%.

Is rising domestic ownership good for Meesho stock?

Generally yes. Domestic institutions tend to hold through volatility, reducing sharp price swings. It also signals local investor confidence and reduces dependence on foreign capital flows.

How much of Meesho became tradeable after the lock-in expired?

Approximately 68% of outstanding equity became eligible for trading after June 9, according to Nuvama Alternative & Quantitative Research.

Did SoftBank or Prosus sell their Meesho shares?

No. Peak XV Partners, SoftBank, Prosus, Elevation Capital, and RPS Ventures retained their holdings during the June quarter.

Need Help Implementing This?

Tracking shareholding patterns, institutional flows, and ownership transitions requires structured data pipelines. If your fintech team needs help building real-time cap table monitoring or investor analytics dashboards, reach out to the Logicity team.

Source: Inc42 Media / Akshit Pushkarna

Huma Shazia

Senior AI & Tech Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.