Key Takeaways

- Unscoreable borrowers perform like 600-639 credit tier, not deep subprime as assumed

- Top-tier 'Thrivers' grew 32% while middle class shrank 6% over two years

- Job tenure under 6 months correlates with 40% higher delinquency rates

Consumer lenders face a brutal paradox in 2026: growth pressure is intense, but auto and credit card delinquencies sit near Great Recession highs. New data from Equifax suggests the standard playbook is broken. Lenders auto-declining thin-file applicants are rejecting a population that actually performs like near-prime borrowers, not subprime risks.

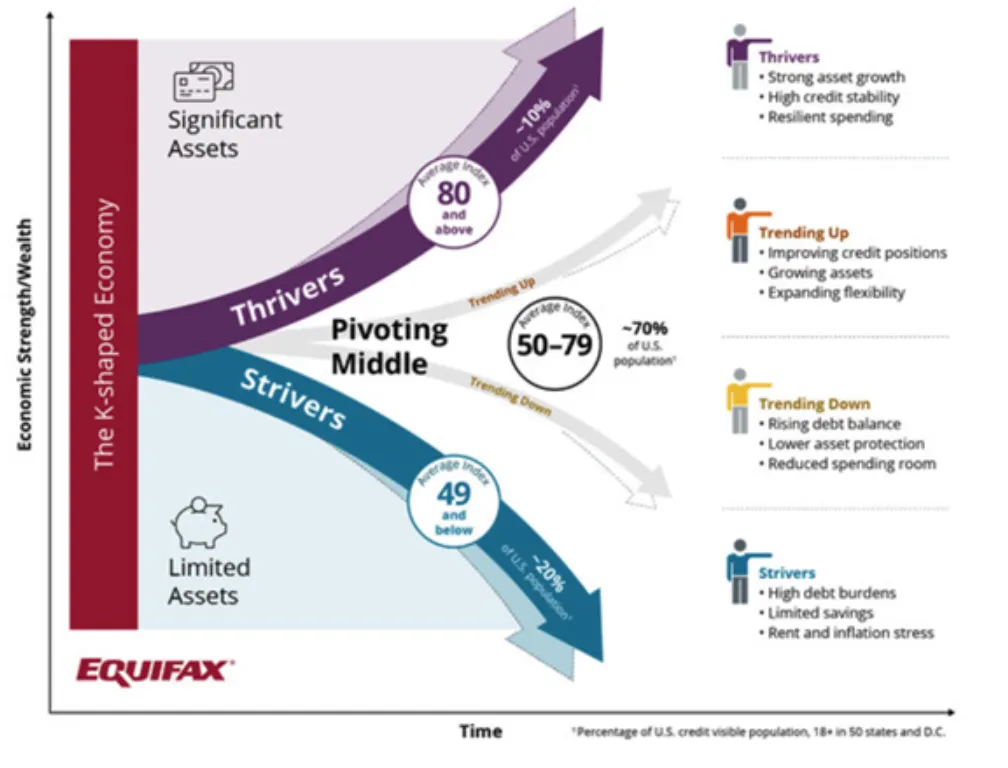

The core problem is a K-shaped economy where consumer financial health is splitting sharply. The top tier is thriving. The middle is shrinking. And traditional credit scores, designed for more uniform conditions, cannot tell the difference between a high-income professional with no credit history and a genuine subprime risk.

What does K-shaped economy mean for lenders?

Equifax's Market Pulse data shows the U.S. consumer base actively splitting over the past two years. The "Thrivers," the top economic tier, grew by 32% and now represent just over 10% of the population. Meanwhile, the traditional middle class shrank 6%. At the bottom, "Strivers" increased 11%, now comprising roughly 20-21% of consumers.

If you only write loans for the top tier, you are fighting over a shrinking pool. The growth opportunity sits in the middle and lower segments. The question is how to say yes safely.

The thin-file myth costs lenders real revenue

For years, lenders operated on a simple rule: no score, no loan. The assumption was that unscoreable applicants perform like deep subprime risks. Equifax studied over 9 million card originations and found this assumption is wrong.

The unscoreable and thin-file population performs remarkably close to the 600-639 credit band. That makes them near-prime, not subprime. By auto-declining this segment, lenders leave substantial portfolio growth on the table. An estimated 45 million Americans are "credit invisible" with thin or no credit files that traditional scores miss entirely.

In a poll of risk, underwriting, and lending leaders during an Equifax webinar, 32% cited lack of additional data as their primary roadblock when evaluating thin-file applicants claiming high stable income. Another 24% worried about data accuracy and authenticity. 13% admitted they simply do not evaluate this segment at all.

How alternative data separates real risk

Two applicants with identical 699 credit scores are not identical risks. When you overlay income verification, employment tenure, and job stability onto traditional credit files, risk profiles diverge dramatically.

Across every credit tier, higher verified income correlates directly with lower delinquency. This goes beyond self-reported numbers. A borrower with a 550 score and strong, verified payroll data can perform like a 600-score borrower.

Employment tenure matters too. Delinquency rates run roughly 40% higher for individuals employed six months or less compared to those with over five years at their current job. Payment stability tracks job stability.

The sharpest risk indicator may be active versus inactive job transitions. When an applicant has an "inactive" payroll record, indicating a job gap or transition in the past year, their delinquency risk jumps by up to 40%.

Why friction is not always the enemy

Consumer lending treats friction as a dirty word. Everyone wants fast, frictionless experiences. But some friction is intelligent. In a K-shaped economy with bifurcated risk, the lenders who win will be those who add strategic verification steps, not those who eliminate all barriers.

This means building layered "swap-in" strategies. Use automated payroll verification. Check job tenure. Verify income through actual employer data rather than self-reported figures. The goal is not more paperwork. It is better data at the right moments.

Manual verification still creates bottlenecks. 15% of lenders in the Equifax poll cited slow verification as a major obstacle. The answer is automated alternative data, not manual document review.

What this means for tech-driven lending platforms

For fintechs and digital lenders, the K-shaped economy creates an arbitrage opportunity. Traditional banks often lack the data infrastructure to segment thin-file populations effectively. Platforms that integrate payroll APIs, employment verification, and income data can approve borrowers that legacy institutions decline.

The technology stack matters. Real-time payroll data beats static credit reports. Employment databases that track active versus inactive status provide risk signals traditional bureaus cannot match. Lenders building these integrations now will capture market share as the middle class continues to contract.

Logicity's Take

Equifax has obvious commercial interest here. They sell the alternative data products they recommend. But the underlying data is hard to argue with. If thin-file borrowers really perform like near-prime rather than subprime, auto-declining them is leaving money on the table. The competitive pressure will force adoption. Lenders using tools like Plaid for payroll verification or Argyle for employment data already have an edge. Those still relying purely on FICO scores will find their addressable market shrinking alongside the middle class. The question is not whether to integrate alternative data, but how fast.

Frequently Asked Questions

What is a K-shaped economy?

A K-shaped economy describes an uneven recovery where upper-income households with assets and job security recover quickly, while lower-income workers continue struggling with inflation, stagnant wages, and depleted savings. The divergence creates two distinct consumer segments with very different risk profiles.

How do thin-file borrowers actually perform on loans?

Equifax data from 9 million card originations shows thin-file and unscoreable borrowers perform close to the 600-639 credit tier. This makes them near-prime risks, not subprime as traditionally assumed.

What alternative data helps lenders assess thin-file applicants?

Key data points include verified payroll income, employment tenure, job stability indicators, and active versus inactive employment status. These signals correlate strongly with delinquency risk across all credit tiers.

How much does job tenure affect loan delinquency?

Borrowers employed six months or less show approximately 40% higher delinquency rates compared to those with over five years at their current employer.

How governments are adopting AI tools for decision-making

Need Help Implementing This?

If you are building lending products and need help integrating payroll APIs, employment verification, or alternative data scoring, reach out to the Logicity team. We cover the tools and vendors that matter.

Source: Banking Dive

Huma Shazia

Senior AI & Tech Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.