Key Takeaways

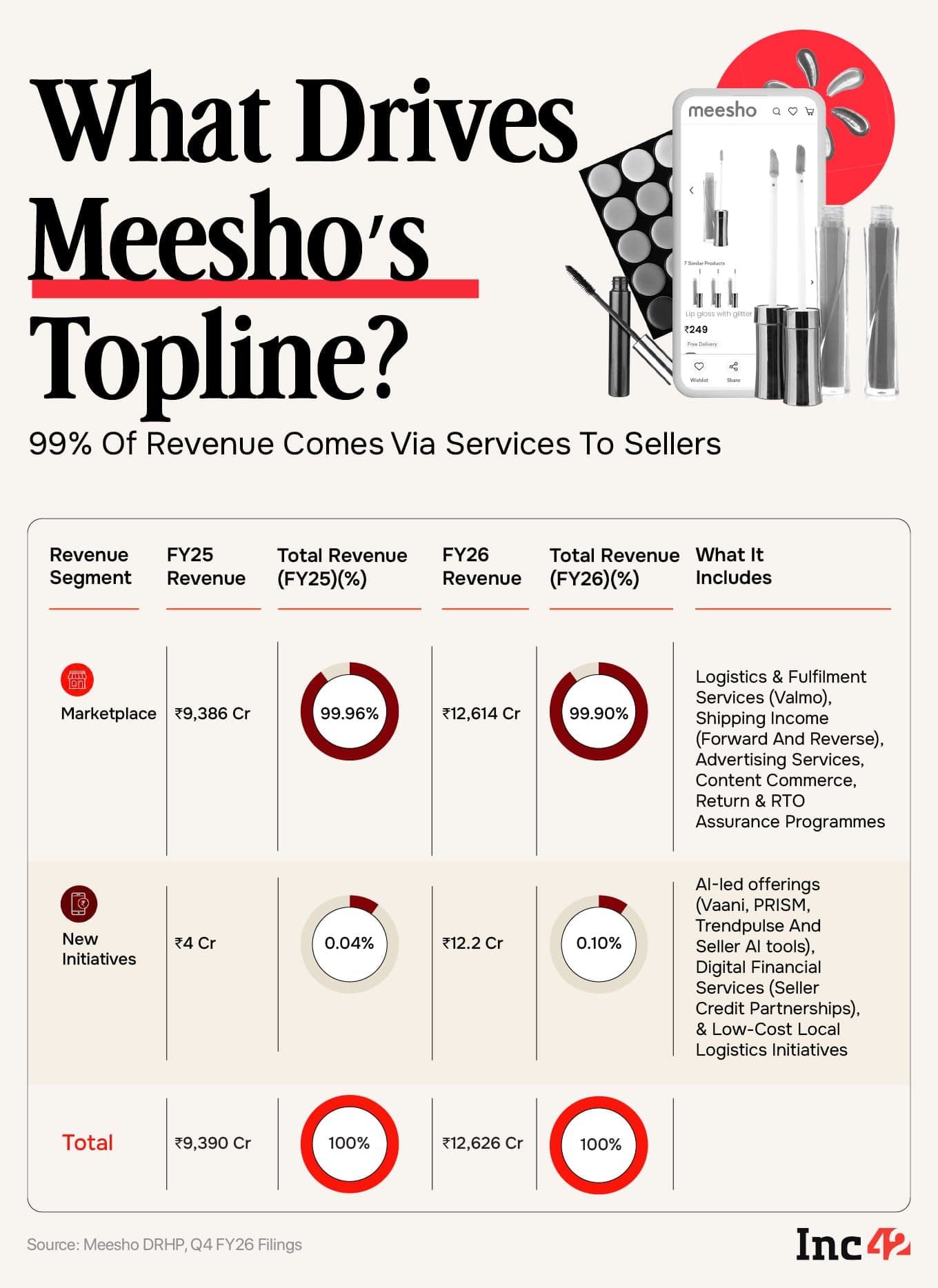

- Meesho earns ₹12,626 Cr annually without charging sellers any commission on orders

- Revenue comes from logistics (Valmo), advertising tools, and seller-facing services instead

- The company targets Tier III-IV India with unbranded, low-price goods, serving 264 million annual users

Meesho generated ₹12,626 Cr in revenue from operations in FY26 without charging sellers a single rupee in commission. That sentence should make any fintech professional pause. The Bengaluru-based marketplace, which went public in December 2025 after raising ₹5,400 Cr through its IPO, has built something structurally different from Amazon or Flipkart. Every saree, kitchen organiser, or bedsheet sold on the platform earns Meesho nothing directly from the transaction itself.

So how does a marketplace serving 264 million annual transacting users and 9.6 lakh sellers turn a profit? The answer lies in a UPI-style monetisation strategy: use the transaction as a lever, not a toll booth.

Why Meesho abandoned the commission model

Most ecommerce marketplaces follow a simple formula. Sellers list products, customers buy them, and the platform takes a cut. Higher order values mean higher revenue. Meesho's founders, IIT Delhi alumni Vidit Aatrey and Sanjeev Barnwal, concluded this model wouldn't work for their target market: small merchants selling unbranded goods at ₹200-500 price points to customers in Tier III, IV, and beyond.

These sellers operate on razor-thin margins. A 15-20% commission, standard across Indian marketplaces, would either price them out or force them to inflate prices, defeating the purpose of serving value-conscious buyers. Meesho's solution was counterintuitive: charge nothing on the transaction, then monetise everything around it.

"We want to democratize internet commerce for everyone in India, not just the top 50 million users," Aatrey has said in interviews. That thesis survived the company's pivot from social commerce (reselling via WhatsApp) to a full marketplace model, and it survived the pandemic. After $1.4 Bn in funding from SoftBank, Prosus, Peak XV, and Meta, it's now being tested in public markets.

The three revenue engines that replace commissions

Meesho's marketplace segment contributed ₹12,614 Cr in FY26, accounting for 99.9% of total operating revenue. That revenue comes from three distinct service layers wrapped around every transaction.

First, logistics. Meesho operates Valmo, its logistics platform that coordinates with third-party carriers to move orders across India's 28,000+ pin codes. Sellers don't need their own distribution network. They pay Meesho shipping charges based on product weight, delivery zone, and payment mode. When the product reaches the customer, Meesho books forward shipping income. When orders get returned, it earns return shipping income for getting the product back to the seller.

Second, advertising. Sellers can pay to boost visibility for their listings. This is the same playbook Amazon and Flipkart use, but on Meesho's platform it's the primary revenue driver rather than a supplement to commissions.

Third, seller services. Meesho offers financial services, AI-powered tools, and operational support to merchants. The company is betting on these adjacent streams to expand revenue per seller without touching the core transaction.

The unit economics question

Can this model sustain profitability at scale? Meesho achieved operating profitability in Q2 FY24, a rare milestone among Indian ecommerce players. But the company's margins depend on logistics efficiency and advertising uptake, both of which face pressure.

Logistics costs scale with order volume. Unlike commissions, which are percentage-based and rise with order value, shipping income is fixed per delivery. A ₹200 order costs roughly the same to deliver as a ₹500 order, but the revenue potential from ancillary services is lower. Meesho needs high order frequency per seller to make the economics work.

Advertising revenue depends on seller sophistication. Small merchants in Tier II-IV cities may not immediately understand or trust paid promotion tools. Meesho has been investing in AI-powered services to lower that barrier, but adoption rates will determine how quickly ad revenue scales.

How this compares to fintech transaction models

The Inc42 analysis draws a useful parallel: Meesho's approach resembles UPI-reliant fintech apps. Companies like PhonePe and Paytm earn little or nothing on the core payment transaction. Their revenue comes from cross-selling financial products, merchant services, and advertising to users already on the platform.

Meesho is applying the same logic to commerce. The transaction is the hook. Revenue comes from owning the infrastructure around it. This model rewards platforms that can increase transaction frequency and deepen seller relationships, rather than those chasing higher order values.

For fintech teams evaluating partnerships or competitive positioning, Meesho's approach offers a template. Zero-margin core products can work if the surrounding services have clear monetisation paths and low marginal costs.

What comes next

Meesho is betting on AI-powered services, financial products for sellers, and hyperlocal logistics as its next growth vectors. The company's IPO filing indicates plans to expand Valmo's capabilities and deepen its fintech offerings.

The question is whether small sellers will pay for these services at rates that justify the investment. Meesho's advantage is lock-in: once a seller relies on Valmo for logistics and Meesho's dashboard for visibility, switching costs rise. The disadvantage is that these sellers are price-sensitive by definition. Monetising them requires finesse.

Logicity's Take

Meesho's model is a case study in reframing where value gets captured. By making the transaction free, the company positioned itself as the default choice for India's long tail of small merchants, many of whom would never pay Amazon or Flipkart's commission rates. The bet is that logistics and advertising revenue, combined with financial services, will eventually exceed what commissions would have generated. For fintech teams, the parallel to UPI apps is instructive: owning the transaction graph creates monetisation options that don't exist for platforms with transactional revenue models. Meesho's public market performance will test whether this thesis holds outside of private market valuations.

Frequently Asked Questions

How does Meesho make money without commissions?

Meesho earns revenue through logistics services (shipping and returns via Valmo), advertising tools for sellers, and financial/operational services. The transaction itself is free for sellers.

What is Meesho's annual revenue?

Meesho reported ₹12,626 Cr in revenue from operations in FY26, with 99.9% coming from its marketplace segment.

Is Meesho profitable?

Meesho achieved operating profitability in Q2 FY24. Long-term margins depend on logistics efficiency and seller adoption of paid advertising tools.

How many sellers does Meesho have?

Meesho works with over 9.6 lakh (960,000) sellers as of FY26, primarily small merchants selling unbranded goods.

How is Meesho different from Amazon and Flipkart?

Meesho charges no seller commissions, targets Tier III-IV cities with low-price unbranded goods, and monetises through services rather than transaction fees.

Need Help Implementing This?

If you're building a marketplace or fintech product and want to explore zero-commission or service-led monetisation models, Logicity's team can help you map unit economics and identify viable revenue streams. Get in touch at logicity.in/contact.

Source: Inc42 Media / Palak Sharma

Manaal Khan

Tech & Innovation Writer

Produced with AI assistance and reviewed by the Logicity editorial team. Learn more in our Editorial Policy.