8 Stripe Alternatives Tested: Which Payment Processor Fits?

Key Takeaways

- Merchant of Record services like Paddle handle global tax compliance for a flat 5% fee, eliminating the SaaS 'hidden tax' problem

- Multi-currency platforms like Airwallex can cut FX and cross-border costs by up to 80% compared to traditional gateways

- Interchange-plus pricing from Helcim beats flat-rate models for businesses processing over $10,000 monthly

Your payment processor shapes two things that matter: customer experience and cash flow. When it fails, your reputation takes the hit at the worst possible moment. Stripe has been the default for online payments for years, but the landscape in 2026 looks different. More options exist, and many solve problems Stripe either ignores or charges extra to fix.

The Zapier team spent dozens of hours testing payment platforms. Combined with real-world experience running small business invoicing, a clear picture emerges: the right alternative depends entirely on your specific pain point. Chasing lower fees? Need physical POS? Drowning in international tax compliance? Each problem has a different answer.

The 8 Best Stripe Alternatives in 2026

- PayPal — for easy payment setup

- Paddle — for merchant of record services

- Adyen — for global enterprises

- Shopify Payments — for eCommerce stores

- Square — for selling online and offline

- Helcim — for interchange pricing

- PayPal Enterprise Payments — for consolidating payment methods

- Airwallex — for cross-border businesses

What Makes a Good Stripe Alternative?

Three criteria separate the contenders from the pretenders. First, pricing structure. Does the platform offer flat-rate, interchange-plus, or subscription-based pricing? The model should be transparent and not balloon costs as transaction volume grows. Second, functionality. Does it handle recurring billing, physical point-of-sale, or merchant of record services? Top contenders manage compliance and administrative work so you can focus elsewhere. Third, integrations. No silos allowed. A good processor offers developer-friendly APIs, native connections, or Zapier integration.

“The era of the 'one-size-fits-all' payment processor is over. 2026 is about intelligent orchestration—routing payments where they succeed most and cost the least.”

— Elena Rossi, Fintech Infrastructure Analyst at Global Payments Research

PayPal: The Easy Setup Option

PayPal remains the fastest path from zero to accepting payments. No complex API integration required. For businesses just starting out or those wanting to add a trusted payment option alongside existing methods, PayPal's brand recognition drives conversions. The platform reports a 15% average increase in checkout conversion rates when businesses add PayPal or Braintree to existing card-payment flows.

The tradeoff: PayPal's flat-rate pricing becomes expensive at scale. High-volume merchants will find better rates elsewhere.

Paddle: The SaaS Tax Compliance Solution

Paddle operates as a Merchant of Record, meaning they become the legal seller of your software. This shifts global tax collection, compliance, and fraud management entirely off your plate. For SaaS companies, this solves what HackerNews discussions call 'the hidden tax' problem: the mounting costs of Stripe add-ons like Stripe Tax and Radar.

“For SaaS startups, Stripe is the easy button until you reach $1M in revenue. Then, the tax and regulatory overhead makes a Merchant of Record service the only logical choice.”

— David Chen, Head of Growth at a leading SaaS consultancy

Adyen: Enterprise-Grade Global Infrastructure

Adyen targets large enterprises processing payments across multiple countries. The platform supports AI-powered smart routing that automatically switches providers in milliseconds to minimize cost and maximize approval rates. This matters when you're processing millions in transactions and a 1% improvement in approval rates translates to significant revenue.

The catch: Adyen's enterprise focus means smaller businesses won't get the attention or pricing they need. This is a platform for companies already processing at scale.

Shopify Payments: Native eCommerce Integration

If you're already on Shopify, their native payment solution eliminates the friction of third-party integrations. Transaction fees drop compared to using external processors, and everything lives in one dashboard. The limitation is obvious: this only makes sense if Shopify is already your eCommerce platform.

Square: Bridging Online and Offline Sales

Square built its reputation on physical point-of-sale hardware, but the platform now handles online payments equally well. For businesses selling both in-person and online, Square provides unified reporting and inventory management. Restaurants, retail stores, and service businesses with physical locations find particular value here.

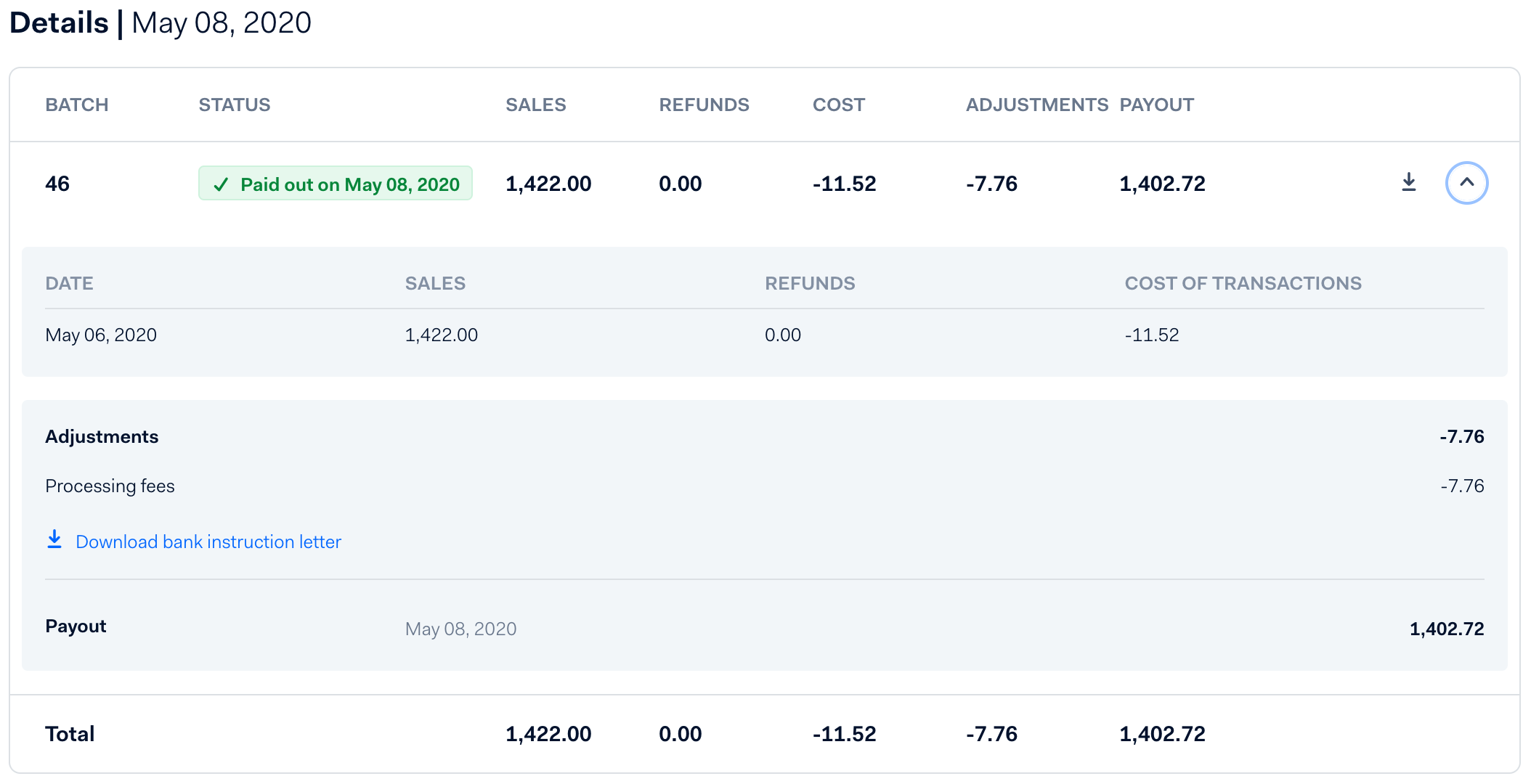

Helcim: Transparent Interchange Pricing

Helcim uses interchange-plus pricing, which means you pay the actual card network fee plus a small margin. This model beats flat-rate processors for businesses processing over $10,000 monthly. The transparency appeals to businesses frustrated by opaque fee structures. HackerNews discussions frequently recommend Helcim specifically for those who want to understand exactly where their money goes.

PayPal Enterprise Payments: Consolidating Methods

PayPal Enterprise, powered by Braintree, lets larger businesses accept cards, PayPal, Venmo, and alternative payment methods through a single integration. The value proposition is consolidation: one dashboard, one reconciliation process, multiple payment options for customers.

Airwallex: Cross-Border Without the FX Pain

Airwallex targets businesses selling internationally. The platform offers multi-currency wallets that let you hold, pay, and receive in multiple currencies without forced conversions. For high-volume merchants, this can cut FX and cross-border costs by up to 80% compared to traditional gateways that convert everything to your home currency.

Global eCommerce businesses benefit most. If you're selling primarily to domestic customers, the cross-border advantages won't matter.

Comparison: Finding Your Fit

| Platform | Best For | Pricing Model | Key Advantage |

|---|---|---|---|

| PayPal | Quick setup | Flat-rate | Brand recognition, 15% conversion boost |

| Paddle | SaaS companies | 5% MoR fee | Full tax compliance handled |

| Adyen | Enterprise | Volume-based | AI-powered smart routing |

| Shopify Payments | Shopify stores | Flat-rate | Native integration |

| Square | Omnichannel retail | Flat-rate | Unified POS + online |

| Helcim | Cost-conscious | Interchange-plus | Transparent pricing |

| PayPal Enterprise | Multi-method | Volume-based | Payment consolidation |

| Airwallex | International | FX + fees | 80% cross-border savings |

The Decision Framework

Switching payment processors is not trivial. Migration takes time, and customers notice if something breaks. But staying with an ill-fitting processor costs money every month. The key questions:

- Are you spending more than 30 minutes monthly on tax compliance? Consider Paddle.

- Do you sell in 3+ countries with different currencies? Airwallex likely saves money.

- Processing over $10,000 monthly? Interchange-plus pricing from Helcim probably beats flat rates.

- Running a Shopify store? The native payment option reduces friction.

- Need unified online and physical sales? Square handles both.

Logicity's Take

Frequently Asked Questions

When should I switch from Stripe to a Merchant of Record like Paddle?

Most SaaS companies find the switch makes sense around $1M in annual revenue. At that point, the time spent on global tax compliance and the cost of Stripe's add-on services like Stripe Tax typically exceeds Paddle's 5% flat fee.

What's the difference between flat-rate and interchange-plus pricing?

Flat-rate means you pay the same percentage on every transaction regardless of card type. Interchange-plus means you pay the actual card network fee (which varies by card) plus a fixed margin. Interchange-plus usually costs less for businesses processing over $10,000 monthly.

Can I use multiple payment processors at once?

Yes. Many businesses use smart routing to send transactions to whichever processor offers the best approval rate or lowest cost for that specific transaction. This adds complexity but can improve margins at scale.

How much can Airwallex save on international transactions?

Airwallex reports up to 80% reduction in FX and cross-border costs for high-volume merchants, primarily by allowing businesses to hold multi-currency wallets instead of forcing conversion to a home currency on every transaction.

Is Stripe still the best option for startups?

For most early-stage startups, yes. Stripe's documentation, ease of integration, and comprehensive feature set make it the fastest path to accepting payments. The alternatives become more compelling as specific needs emerge at scale.

Another in-depth software comparison testing multiple options for specific business needs

Need Help Implementing This?

Source: The Zapier Blog

Manaal Khan

Tech & Innovation Writer

اقرأ أيضاً

رأي مغاير: كيف يؤثر اختراق الأمن الداخلي الأميركي على شركاتنا الخاصة؟

في ظل اختراق عقود الأمن الداخلي الأميركي مع شركات خاصة، نناقش تأثير هذا الاختراق على مستقبل الأمن السيبراني. نستعرض الإحصاءات الموثوقة ونناقش كيف يمكن للشركات الخاصة أن تتعامل مع هذا التهديد. استمتع بقراءة هذا التحليل العميق

الإنسان في زمن ما بعد الوجود البشري: نحو نظام للتعايش بين الإنسان والروبوت - Centre for Arab Unity Studies

في هذا المقال، سنناقش كيف يمكن للبشر والروبوتات التعايش في نظام متكامل. سنستعرض التحديات والحلول المحتملة التي تضعها شركات مثل جوجل وأمازون. كما سنلقي نظرة على التوقعات المستقبلية وفقًا لتقرير ماكنزي

إطلاق ناسا لمهمة مأهولة إلى القمر: خطوة تاريخية نحو استكشاف الفضاء

تعتبر المهمة الجديدة خطوة هامة نحو استكشاف الفضاء وتطوير التكنولوجيا. سوف تشمل المهمة إرسال رواد فضاء إلى سطح القمر لconducting تجارب علمية. ستسهم هذه المهمة في تطوير فهمنا للفضاء وتحسين التكنولوجيا المستخدمة في استكشاف الفضاء.